If you are experiencing mortgage stress, now’s the time to get on the front foot with your lender. As your mortgage broker, we can help you prepare and plan for the unknown.

It’s no surprise that the outbreak of COVID-19 has caused a huge increase in mortgage stress. According to the Australian Banking Association (ABA), more than 485,000 mortgage repayments were deferred between February and June this year.

IS THE CLIFF COMING?

Experts and commentators have been warning us of the impending cliff that’s coming. Lenders have been giving borrowers a pause on their mortgage repayments. These breaks were due to end soon, but with the support of APRA, lenders have recently announced an extension of deferrals until the end of March 2021. At the same time, JobKeeper and JobSeeker programs were only promised until September. Fortunately, JobKeeper and JobSeeker are not coming to a sudden stop. There is now a clearer outline of the next stages, allowing people to better prepare for what may come next.

A MORE GRADUAL REDUCTION IN SUPPORT.

JobKeeper and JobSeeker were announced early on in the Government’s response to the unfolding crisis. What would happen after the first six months wasn’t announced and everyone’s fear was that the end of the assistance would be devastating. The schemes have been widely regarded as a success and fortunately the Government is looking at a more gradual reduction in payments. At this stage, the JobKeeper payment will continue to be available to eligible businesses until March 28.

JobKeeper will be being reduced in two steps. From the end of September, full-time employees will go from $1,500 a fortnight to $1,200. And then, at the beginning of the new year on January 3, it will drop to $1,000 a fortnight.

For part-time workers, which is people working fewer than 20 hours a week in February this year, JobKeeper will be halved to $750 a fortnight from the end of September. In the new year it will make a less drastic reduction to $650 a fortnight.

If you’re receiving JobKeeper, it’s not an automatic transition to the new amount. Businesses and employees will need to apply for the extension after the initial JobKeeper finishes on September 28. Once again, employers and sole traders will have to demonstrate a 30 or 50 per cent reduction in turnover, depending on the size of their turnover, in the September quarter (compared with the same period in 2019). The second extension will commence on January 3. To qualify for this stage, a business will need to show a loss for the December quarter.

It’s also worth noting that the JobKeeper payment will continue to be made available to new recipients, as long as they meet the eligibility requirements and the turnover tests that apply during the relevant JobKeeper payment period.

JobSeeker is also changing. The $550 coronavirus supplement paid each fortnight is being reduced to $250, but the base rate is staying the same. So, the total payment will go from $1,115 down to $815.

To make up for this reduction, the Government is allowing those on JobSeeker to earn $300 a fortnight, up from the current $106. The intention is to encourage people to get out and get work, without having to worry about losing their financial support. And, from the beginning of August this year, you’ll have to actively be looking for work to stay on JobSeeker.

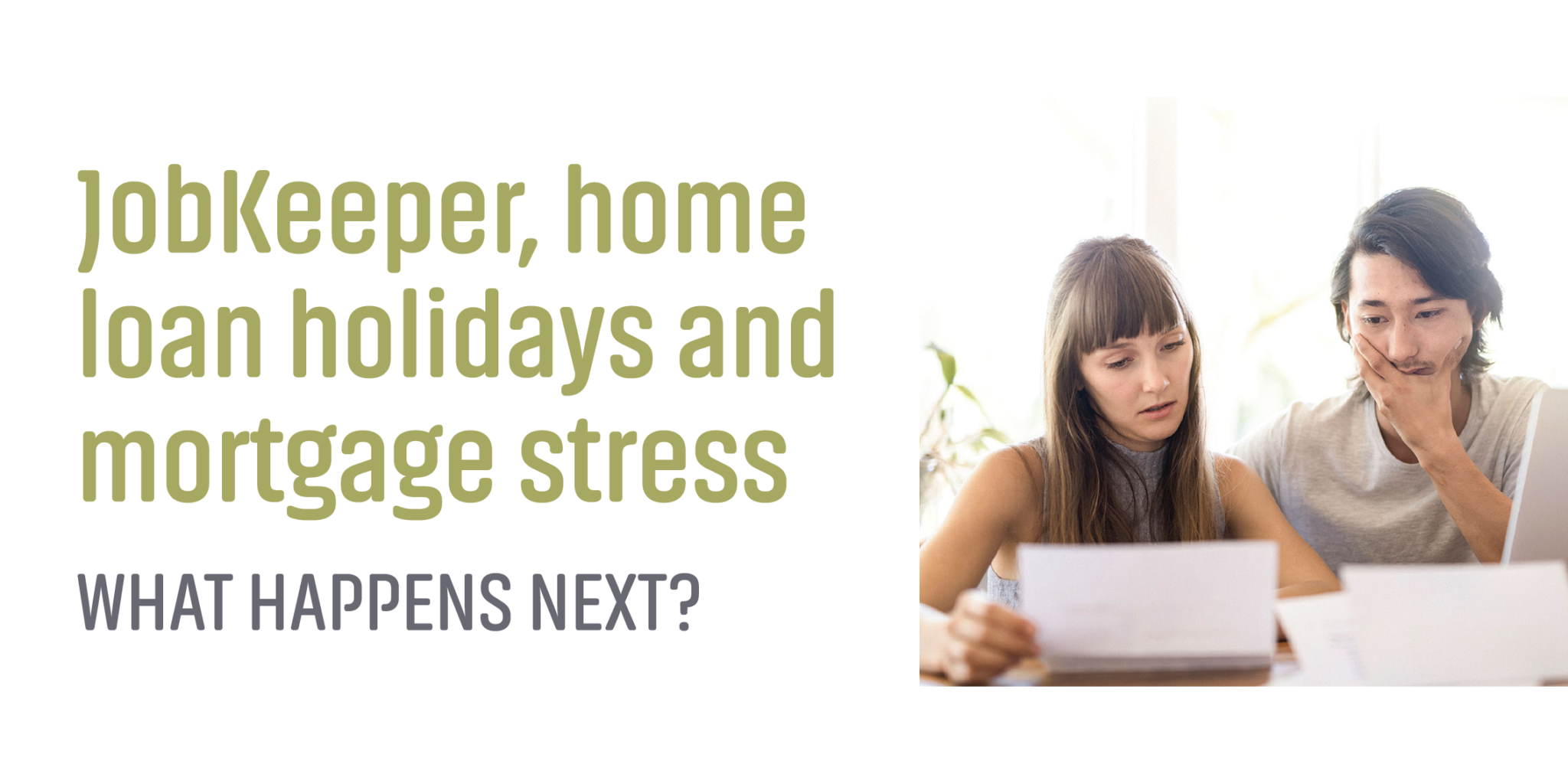

HOW WILL YOU FEEL AFTER A MORTGAGE HOLIDAY?

Like many people you may have taken up your lender’s offer of a mortgage repayment pause. While this can certainly help in the short-term, there are long-term ramifications you should watch out for. The lenders aren’t just giving you these payments for free. Instead, the amount of interest you missed is getting added on to the principal of the loan. This is called interest capitalisation.

In short, after the mortgage pause you will have a bigger loan and your repayments will likely be more than before the ‘holiday’. And things like monthly fees (based on the size of your loan) could be added to your loan balance.

HOW CAN YOU AVOID MORTGAGE STRESS?

Your circumstances are unique, and our world is shifting week to week. Changes in the economy, society, health, employment and government support will affect every one of us in different ways. Knowing how government support is being delivered is one thing. If you are receiving this support, it can help you plan for the next few months. But there are many other things you can do to protect your financial well-being and avoid mortgage stress. For instance, should you swap to an interest-only loan? With interest rates at a historic low, is it a good time to fix your loan? Or split your loan? Or is there a more suitable loan out there that could help save you money? Maybe you’re fortunate enough not to have had an income loss during this time and therefore might be considering opportunities to invest in the property market.

In these times, it’s a good idea to reach out and get help. And that’s why we’re here. We can answer your questions and look at your circumstances to make sure you’re prepared for what could be coming next. This could mean refinancing or approaching your lender for a better rate. Because we do this type of work every day, we have a pretty good idea what lenders can do to win or keep your business.

While sometimes it can feel like things are out of our control, you can take control of your mortgage. Get in touch and we can help you find the financial product that’s right for you, right now.